‘If you could forthwith provide 150,000 low-income young people across the UK with over £400 million at no cost to Government, would you take action?’

The question on The Share Foundation’s invitation to MPs

![]()

A couple of weeks ago, we welcomed the introduction of Trump Accounts for young people in American families; but we noted the absence of a process for Government opening where family opening does not take place. In order to deal with this challenge, HMRC allocation was a key part of Gordon Brown and Ruth Kelly's Child Trust Fund design. 28.4% of accounts were opened in this way: that’s for 1.74 million young people, and the proportion from low-income backgrounds was 70% higher in this segment than for family-opened accounts.

This high proportion of disadvantage is why Governments have to take action if they want to break the cycle of deprivation. Tony Blair's Government understood that well, and Chancellor George Osborne also got the message from The Share Foundation, Barnardo’s and Action for Children, when he agreed to provide Junior ISAs for all young people in care for at least one year: the scheme which The Share Foundation has been running for the past fourteen years on behalf of the Department for Education.

The fact is that Government knows who are the young people threatened by the cycle of deprivation: public bodies are the only reliable source of information, and they must therefore take action.

However, there are two other major responsibilities which come with opening these accounts: they must be monitored throughout the child's journey towards adulthood, and they must be delivered when the time is right.

Unfortunately the monitoring and delivery of HMRC-allocated Child Trust Funds did not receive the same attention as their opening, and that's why The Share Foundation estimates that there are £1.2 billion of these now adult-owned accounts sitting dormant with account providers, rather than helping their young owners to achieve their potential in adult life. It's estimated that the proportion of these unclaimed accounts is four times higher than for family-opened Child Trust Funds.

There are now ten HMRC-allocated account providers, and it's thought that all except NatWest are charging the maximum fee of 1.5%: that's nearly £20 million annually in fees. They speak warmly of trying to find their account owners, but in practise they do very little to achieve this, again with the exception of NatWest.

As the trust ‘settlor’, HMRC should have required records to be maintained of which accounts were HMRC-allocated, notwithstanding account provider mergers over the past twenty years; but they failed to do this, and they are still not giving priority to carrying out the analysis in retrospect. It was the discovery at The Share Centre which opened my eyes to the problem: the analysis showed that 86% of these accounts were either never registered or ‘addressee gone away’.

This is why The Share Foundation set up its free search facility, https://findCTF.sharefound.org , in 2018, and so far we've linked 139,000 applicants with £311 million of accounts. In 2019 we encouraged and supported the Westminster Hall debate led by Helen Goodman MP, and this is what she had to say about unclaimed low-income Child Trust Funds:

‘But for those children from families on Child Tax Credit, the worst-off, struggling families in the lowest 15% of the income distribution there is no contact information for four out of ten of them, and The Share Foundation tell me that on top of that another 40% have been contacted but have not responded. So this is something between 400,000 and 800,000 children with accounts valued at £1,600 — a lost value of £710 million or even £1.4 billion. This is completely disgraceful.’

Therefore the monitoring of which accounts are HMRC-allocated is fundamentally important. 96% of those 139,000 applicants linked through The Share Foundation’s search facility were administered by HMRC-allocated account providers: this bears out our estimate that the unclaimed rate for these accounts is so much higher than for family-opened accounts.

Of course, there are considerable differences in the proportion of HMRC-allocated and low-income Child Trust Funds across the country, as the analysis in the right-hand column shows. The worst affected areas are the devolved nations — Wales, Scotland and Northern Ireland — and the northern regions of England (including the north-west: Andy Burnham, please take note).

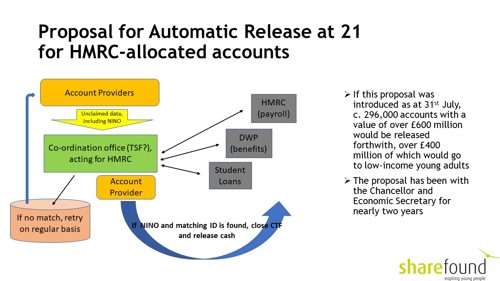

With 71% of Child Trust Fund owners now having reached adulthood, and with half of these being aged between 21 and 23, the emphasis now needs to be placed on delivery. This is why The Share Foundation has been pushing so hard for the ‘Automatic Release at 21’ process for HMRC-allocated accounts to be introduced over the past two years. They estimate that the system would immediately release £600 million-worth of accounts for nearly 300,000 young people, two-thirds of which would go to low-income young people, in order to transform their lives.

This is how the proposal would operate:

The Share Foundation estimates that 62.7% of all unclaimed CTFs are HMRC-allocated, compared to 28.4% at issue. This process would allow three years for a young person to claim or manage their account, after which the majority of unclaimed accounts would be automatically delivered. After the initial catch-up, we estimate that it would release a further £0.25 billion each year until 2031.

- CTF account providers with HMRC-allocated account owners who had reached their 21st birthday would identify these unclaimed accounts and notify HMRC of their identity, including their National Insurance Number.

- HMRC would establish whether those individuals are benefit recipients, on a company payroll or in the student loan system, or through any other current relationship involving Government receipt or payment. HMRC would then confirm that the accounts should be closed and the proceeds paid to an HMRC transfer account for onwards payment as appropriate. HMRC would, if at all possible, notify the young adults of their impending receipt. The Share Foundation has offered to manage this operation for HMRC, if that would help.

- All identified accounts for which HMRC have no current links would be informed as such to the account provider, who would re-test on a quarterly basis going forwards.

At least five Economic Secretaries to the Treasury, under both Conservative and Labour administrations, have thus far refused to activate the Automatic Release proposal, citing ‘legal, data and operational issues’.

On the legal aspects, The Share Foundation has sought legal advice and considers that automatic release is not just lawful, but is required to give effect to the various duties on the Government, including not further handicapping those who are already disadvantaged. A two-hour meeting with our barrister and nine HM Treasury staff and lawyers took place on 27th March ’26.

For the data issues, the fact that all Child Trust Funds are directly referenced by the owner’s National Insurance number enables direct access to up-to-date knowledge of these individuals’ contact information through the benefits, payroll and student loan channels. HMRC is now using these channels to write to unclaimed account owners; so it has already accepted this.

In a question tabled in the House of Lords, a suggestion was made in the HMRC response that the scheme was likely to ‘interfere with an individual’s right to manage their own financial affairs’. It is hard to accept this, when these individuals have no knowledge of the existence of their accounts!

So, where are we now?

- HMRC proposes to write to all unclaimed Child Trust Fund owners on reaching 21, using those up-to-date contact details. These letters are not expected to be sent until early ’27.

- A ‘CTF Taskforce’ has been established with account providers and The Share Foundation.

- Given the clear evidence both at formation (lack of family action, hence the HMRC-allocation) and in communications from account providers over the years (for example, The Share Centre’s analysis in 2018) we do not believe that the letter-writing campaign will work for HMRC-allocated and low-income account owners.

We are therefore hoping that the new administration under Andy Burnham will activate ‘Automatic Release at 21’ for HMRC-allocated accounts.

The need for joined-up thinking to accommodate the opening, monitoring and delivery of savings accounts for young people, over a timespan of twenty years, illustrates the challenge of implementing long-term policies with Governments dependent on a maximum five-year electoral cycle.

All the biggest challenges facing humanity, including inter-generational rebalancing and climate change, are, by definition, long-term. That's why we need a second chamber elected on the basis of how people want to see the country — and the world — in fifty years’ time, in order to provide long-term oversight of short-term executive decisions in the House of Commons.

Gavin Oldham OBE

Share Radio