“The wind swept up from over the sea,

Whispering tales of the Free,

Blowing the sand across the beach,

And the foam and the spray from the sea.”

Rodney F. Russell

With less than seven weeks to go before 29th March, the United Kingdom needs to focus on the turbulence ahead. In a couple of months, we will be through the breakwater and out in the open sea beyond the European Union.

What will the open sea look like? I would be surprised if it is not smoothed by a period of transition as per an amended withdrawal agreement, although it is clear that the ratification of any last-minute deal may well extend well beyond 29th March. But if not, how is the UK placed to weather the storm ahead?

This week we look at recent encouraging accounts of business strength, to conclude that we are well-placed for the challenges ahead.

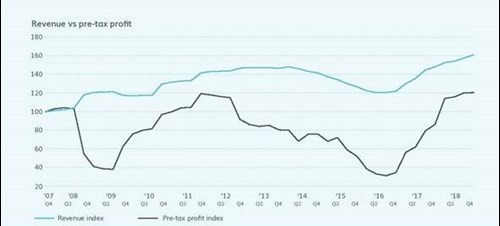

The Share Centre’s quarterly Profit Watch report released last week gave an upbeat assessment of UK businesses, both domestic and international. Nearly all sectors are seeing significant revenue growth, and it is particularly encouraging to see the banking industry slowly emerging from the aftermath of great 2008 financial crash. One of the significant aspects of the chart below is how the tide of both revenue and pre-tax profit changed so clearly for the better following the Brexit referendum, and the consequent fall in £Sterling.

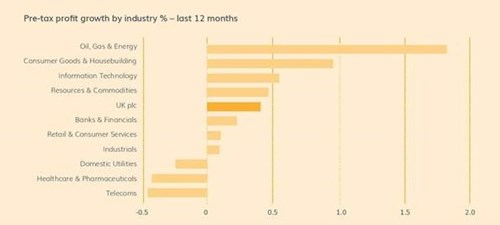

The industry breakdown of pre-tax profit growth over the past 12 months is also encouraging, although the aggregate rate of growth at 1.3% is significantly less than the 10.9% in revenues. Only domestic utilities, healthcare & pharmaceuticals, and telecoms failed to join the party.

UK business is doing well, boosted by the lower pound which has done much to make us more competitive over the past couple of years and to increase the value of repatriated profits earned overseas.

So, while Bank Governor Mark Carney may warn of the weakest UK growth in a decade as he reduces this year’s forecast to 1.2% from the previous 1.7%, we’re in a good place to cope with the rough water ahead.

The challenge is to ensure that all parts of society can share in the strength of the UK economy, as we drew attention to last week. However, we are assured that the Government stands ready to cut taxes and tariffs as necessary to cope with a no-deal Brexit scenario, potentially deploying £15 billion to help boost the economy. This should help considerably.

In contrast, the European Union - and especially the Eurozone - is particularly fragile. Last Wednesday’s Telegraph business section reported, "The slightest shock could tip Eurozone over the edge". Both Italy and France slid deeper into economic contraction in January, and once again Germany did nothing to ease their pain: in fact, quite the reverse, as their finance minister drew up plans for a spending freeze. Guntram Wolff, director of the Bruegel think-tank, said, “The German view is we are not in a recession and we have full employment so there is no need to rely on discretionary spending” and, “Italy is in a self-inflicted recession caused by loose talk”.

Once again, the dysfunctionality of the Eurozone is paraded for all to see. How dare European Commission President Donald Tusk speak of "a special place in hell for Brexiteers without a plan", when he and his colleagues have presided over a single currency area which has no plans for economic recovery for its regional unemployed? How can he not see that it is that very unemployment and regional despair that gave rise to the migration, which has itself caused the Brexit vote in the UK and populism in Italy and France?

As we have warned repeatedly in this commentary, the consequences of Eurozone collapse will be far more serious than Brexit turbulence, and it is just as well that our banking sector is regaining its financial strength in order to cope with the impending crisis.

Meanwhile, the UK should not tie down its global trading prospects by entering or staying in a customs union with the EU, as Jeremy Corbyn has proposed. We need to re-establish our position on the world stage to provide stability, not least so that we are better able to cope and lend strength when the Eurozone does collapse: as it will, unless action is taken by its leaders to integrate politically.

It’s just as well that UK business is so robust in the circumstances.

Gavin Oldham

Share Radio