“That's rich: self-made millionaires less sympathetic to poor.”

Times headline, Tuesday 28 June

![]()

Using inter-generational rebalancing to provide a long-term strategy for social mobility is a key part of the move to a more egalitarian form of capitalism, for which we campaign so passionately. This calls for a systemic change to empower new generations to achieve their potential in adult life, not just a flash in the proverbial political pan.

A research article published in Social Psychological and Personality Science last week, which prompted the above quotation in the Times, proves why it must be systemic and cannot rely on the goodwill of the rich and powerful for its continuance.

Attitudes towards capital have fluctuated for centuries. There are plenty of examples of benevolent patriarchy (for example, the Cadbury family) during the Industrial Revolution, no doubt inspired by their faith. In contrast, some seek to spend in a lavish lifestyle once they have accumulated wealth, and this week’s ‘The Hypnotist’ addresses some of the reasoning behind this.

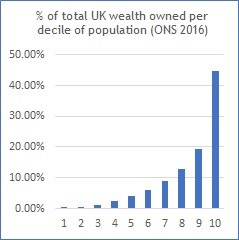

It all goes to show that, if we want a fair and just society where young people have not only the life skills but also some resources to achieve their potential as an adult, we must build the strategy into the structure of our economic governance: much as public health and addressing climate change is accepted by an all-party consensus. The research from Hyunjin Koo and her colleagues shows that we cannot rely on those who have succeeded in their own social mobility to secure the platform for those who have not yet done so: they are more likely to pull the ladder up after them.

I declare an interest as someone who has benefited from family inheritance in order to get going in the first place. My great-grandfather, Arthur Oldham, played a key part in the formation of one of the largest Stock Exchange market makers Wedd Durlacher Mordaunt, which accounted for 40% of all share trading in London in 1986: a firm which I joined in 1976 until it was merged into Barclays.

My father always drew a clear distinction between capital — which was to be stewarded carefully and built up for the benefit of future generations — and income, which could be spent. It's a distinction which has been blurred by our debt-ridden society, since for so many people their main item of capital is the house they live in, and that is supported by massive mortgage debt.

You cannot rely on debt to achieve entrepreneurial success. Not only is it incredibly hard to come by for someone without the collateral to secure it but it also injects a huge dose of additional risk, just exactly at the time when certainty is in such short supply. Of course, you can find those who battle against the odds to achieve self-made millionaire status in spite of this, but they are few and far between. This is why the polarisation of wealth is as great today as it's ever been.

You cannot rely on debt to achieve entrepreneurial success. Not only is it incredibly hard to come by for someone without the collateral to secure it but it also injects a huge dose of additional risk, just exactly at the time when certainty is in such short supply. Of course, you can find those who battle against the odds to achieve self-made millionaire status in spite of this, but they are few and far between. This is why the polarisation of wealth is as great today as it's ever been.

And now Hyunjin Koo and her colleagues tell us that these few extra-ordinary achievers have little sympathy for those who would follow their example, in any case. It's a sad reflection on man’s (because it is usually men we're speaking of) inhumanity to man: they are no doubt prepared to help their own descendants to climb the greasy pole, but have scant regard otherwise for future generations.

But democratic capitalism cannot rely on ‘rich get richer, poor get poorer’ for its continued existence.

If we do not apply a strategic discipline of the kind which we proposed to Michael Gove in February this year, using at least some of the wealth left behind when rich people die to empower disadvantaged young people, the pendulum will swing back towards a heavily-intermediated welfare state which suppresses individual enterprise and individual ownership.

This week’s The Bigger Picture from Professor Tim Evans and Simon Rose deplores the current ‘Politics of Nothingness’ which currently seems to be so endemic and all-encompassing at Westminster. They call for a new sense of strategic purpose, as in the days of Thatcher or Attlee.

Egalitarian Capitalism is that strategic purpose, from an economic perspective. It will bring hope and opportunity for a society deeply challenged by the cost of living crisis, mass automation and social insecurity. Starter capital accounts and incentivised learning fuelled with a degree of hypothecation from inheritance tax receipts will provide a springboard for the young, and ‘Stock for Data’ will provide participation for all in the wealth creation of technology.

We don't need self-made millionaires to make this happen - we just need a sense of strategic purpose, and a systemic commitment.

Gavin Oldham OBE

Share Radio